704.684.4751

- Home

- Products

Small Business

Form 94x Series Form 990 Series Form 1099 Series W-2 Forms ACA Forms ExtensionsAccountant

Tax Professionals

- Support

- Sign In

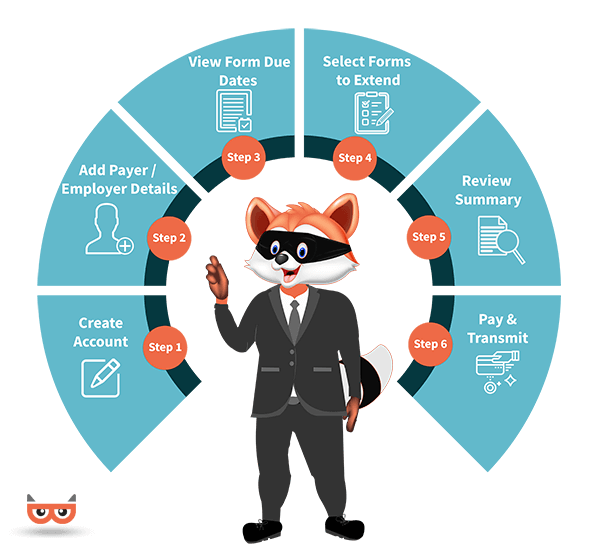

Business Tax Extension Form 7004 is used by Corporations, Entities, Partnership, Limited Liability Company, Certain Estates and Trusts to receive upto 7-months automatic extension to file their return.

| March 15 | Form 1120-S, Form 1065 Series, Form 1041 (Bankruptcy Estate only), Form 3520-A, Form 8804, Form 1042 |

|---|---|

| April 18 | 1120 Series (Excluding Forms 1120-S and 1120-C), Form 1041 (Estate other than a bankruptcy estate) & Form 1041 (Trust) |

| Forms 1041-N, 1041-QFT, 1066 and 706-GS (T) | |

| June 15 | Form 1120 Series (excluding 1120-C), Form 1065 Series, Form 8804 |

| September 17 | Form 1120-C |

Automatic 5-1/2-month extension for An estate (other than a bankruptcy estate) and a trust filing Form 1041.

Automatic extension period for time to file is generally 6 months. Exceptions apply for certain filers of Form 1041 and for C corporations with tax years ending June 30.

C corporations with tax years ending June 30 are eligible for an automatic 7-month extension of time to file (6-month extension if filing Form 1120-POL).

Receive a 5 ½ month Automatic Extension for Certain Estates and Trusts

| Form 1041 (Estate other than a Bankruptcy Estate) | Form 1041 (Trust) |

| Form 706-GS (D) | Form 706-GS (T) | Form 1041 (Bankruptcy Estate only) | Form 1041-N | Form 1041-QFT |

| Form 1042 | Form 1065 | Form 1065-B | Form 1066 | Form 3520-A |

| Form 8612 | Form 8613 | Form 8725 | Form 8804 | Form 8831 |

| Form 8876 | Form 8924 | Form 8928 | - | - |

6-month extension - C-Corporations and Entities with a tax year ending on December 31

7-month extension - Other C-Corporations and Entities with a tax year ending on June 30

6-month extension - If the tax year ends on any month except December 31 and June 30

| Form 1120 | Form 1120-C | Form 1120-F | Form 1120-FSC | Form 1120-S |

| Form 1120-H | Form 1120-L | Form 1120-ND | Form 1120-ND (Section 4951 taxes) | Form 1120-SF |

| Form 1120-PC | Form 1120-POL | Form 1120-REIT | Form 1120-RIC | - |

If you fail to file either a tax extension or tax return within the appropriate deadline (March 15, 2018 for most businesses and April 18, 2018 for most individuals), the IRS will charge interest and penalties on any unpaid Federal taxes.

If you do not file and you owe taxes, the failure-to-file penalty is 5% per month (up to 5 months) of the amount due. If your return is more than 60 days late, you may be subject to a $135 minimum penalty. The IRS will also impose a failure-to-pay penalty of 0.5% per month (up to 25%) of the amount due if you file a return or extension, but don’t pay all your taxes on time.

Conveniently e-file Form 7004 for your business with the Form 7004 mobile app! Download your free app today from the App Store or Google Play.